Analytics in the Lending Marketplace

Authors: Coleman Harris, Allan Mathis, Andreas Puppa

Analytics are Supercharging the Lending Marketplace

The lending marketplace has embraced digital transformation – borrowers are demanding better services for lower fees, while lenders who successfully leverage data have pulled ahead. These institutions utilize analytics to anticipate customer needs and offer personalized financial products. This, in turn, benefits borrowers with more valuable offers tailored to their needs, while lenders can achieve lower expense ratios. Data and analytics levels the playing field of the lending marketplace, providing ample opportunity for small lenders to compete by capitalizing on analytical horsepower.

The Changing Landscape in Lending

Analytical capabilities typically scale with lender size – larger lending institutions have more resources to build teams, capture big data, and perform powerful analytics. This has significantly widened the performance gap between financial institutions, putting firms with small discretionary budgets at a disadvantage.

However, recent advances in the analytics domain have democratized many powerful tools. Open-source data science tools have exploded in popularity, while cloud computing is becoming a more viable option for many data and analytics problems. Leaders like Kaizen capitalize on this opportunity by offering containerized and scalable machine learning solutions, both for data sources that are “big”, and small & wide.

(Did you know? Expense ratios measure how much of a lender’s assets are used for operation)

Continued low rates in the lending industry, coupled with the rapid modernization of the market, have also increased the competitive intensity of lending. Customers can more easily shop around for loans and other financial products, pushing financial institutions to cut margins and find additional revenue sources. Lenders who can leverage data and analytics to consolidate their offerings and chase the economies of scale will be at a considerable competitive advantage moving forward.

Lending Analytics: The Kaizen Perspective

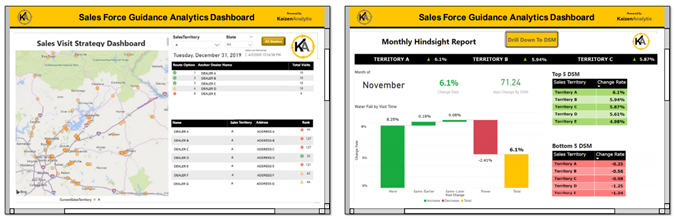

Leveraging data and analytics in the lending space isn’t just limited to the above examples – in many cases, analytics can support multiple functional areas at once. For example, Kaizen Analytix engaged with a provider of auto lending solutions whose business model involved deploying salespeople across the country to various car dealerships who offered auto financing.

Analytics provided optimized solutions for managing loan portfolio performance adjusted for risk, establishing salesperson visit frequency, determining customer segmentation, and managing salesperson route paths. The result from this suite of analytics solutions was a rapid 4% to 6% revenue uplift and enhanced tracking and compliance capabilities.

Graphical user interface, application

Description automatically generated Making timely, intelligent business decisions will continue to be an imperative for lenders. Data and analytics not only help lenders provide optimal terms on loan products to their customers, but also help lenders reach their customers in new and valuable ways, while providing internal process improvements as well.

Deeper Lending Analytics Use Cases

Analytics in lending can provide more than just lower risk and minimized loss. A more comprehensive understanding of a lending institution’s customer base, internal operations, and competitive environment can generate top-line revenue growth, lower expense ratios, greater customer loyalty, and more streamlined processes. Below is a non-exhaustive overview of how analytics is currently benefitting lending institutions.

Increased Credit Risk Accuracy

Advanced artificial intelligence (AI) and machine learning models can learn from myriad points of customer data to improve the accuracy of a customer’s risk assessments. These tools assess both the likelihood of delinquency and the relative costs associated with approving or denying a loan – this optimizes on the risk/return tradeoff, maximizing profitability.

Credit Term Optimization

Analytics tools power lending institutions to customize the loan principal amount, length of the loan, required funds, and interest rate. This both mitigates risk and increases collectable revenue based on the borrower’s unique risk profile. This risk profile can incorporate targeted data related to the individual’s relationship to the lending institution and the external competitive environment.

Fraud Detection

The risk of fraud is commonly cited as one of the biggest concerns for lending institutions, from falsified assets to identity theft. Anomaly detection models and other analytical tools can recognize and deter fraudulent activity before it becomes a serious problem.

Cross-Selling and Capturing Wallet Share

Prediction models using rich customer data improve the targeting and cross-selling of lending offerings, capturing a deeper wallet share among the customer base. For example, analytics tools can accurately predict customer life events like a house purchase, and accordingly offer mortgage loan packages to drive value in both the short and long term.

Workflow Optimization

Easy and intuitive automated processes can aide in new customer acquisition. For example, online banking application abandonment rates can be over 97%. Frictionless onboarding using third party APIs (application programming interfaces) to integrate customer credit scores and collateral valuation are invaluable in customer conversion.

With the modernization of the lending analytics industry, and the growing power of data and analytics tools, it is imperative for lending institutions large and small to incorporate these methodologies into their lending strategies. Whether this involves utilizing small and wide datasets to optimize the way a loan is offered or implementing “big” databases to best segment and target customers, the lending industry is rapidly moving towards data-driven approaches. This democratization of data and analytics tools places small lending firms on the same bleeding edge as large ones – the groups who can best harness this power will come out on top.

More Publications

-

Automotive Innovation Series, Part 4: Harnessing Unsupervised Machine Learning in the Automotive Sector

-

The Future of Payment Infrastructure: Overcoming Challenges & Embracing Innovation

-

The Current State of the Financial Services Industry: Key Challenges & Priorities for the Future

-

The Current State of Credit Unions: Challenges, Trends, and Solutions for Sustainable Growth